In brief - Foreign investors and developers to be affected by stamp duty and land tax surcharges

Foreign investor stamp duty surcharges, which generally apply to transactions involving residential land already subject to stamp duty, were recently introduced in New South Wales and are set to be introduced in Queensland in October, while Victoria will increase its existing surcharge from 1 July 2016. In addition, 2017 will see the introduction of a foreign investor land tax surcharge in New South Wales and an increase on the absentee owner land tax surcharge in Victoria.

Foreign investors may be liable to pay stamp duty or land tax surcharges

Victoria has had a foreign purchaser stamp duty surcharge in place since 1 July 2015. New South Wales and Queensland have followed Victoria's lead and introduced similar surcharges with effect from 21 June 2016 (for New South Wales) and 1 October 2016 (for Queensland). The surcharge in Victoria will increase from 3% to 7% on and from 1 July 2016.

New South Wales has introduced a foreign investor land tax surcharge with effect from the 2017 land tax year. Victoria introduced an "absentee owner" land tax surcharge of 0.5% on 1 January 2016 which will increase to 1.5% on and from 1 January 2017.

Foreign investors should seek advice on whether they are liable to pay the stamp duty or land tax surcharges. The measures will also impact developers who are looking to encourage foreign investors to enter into the market.

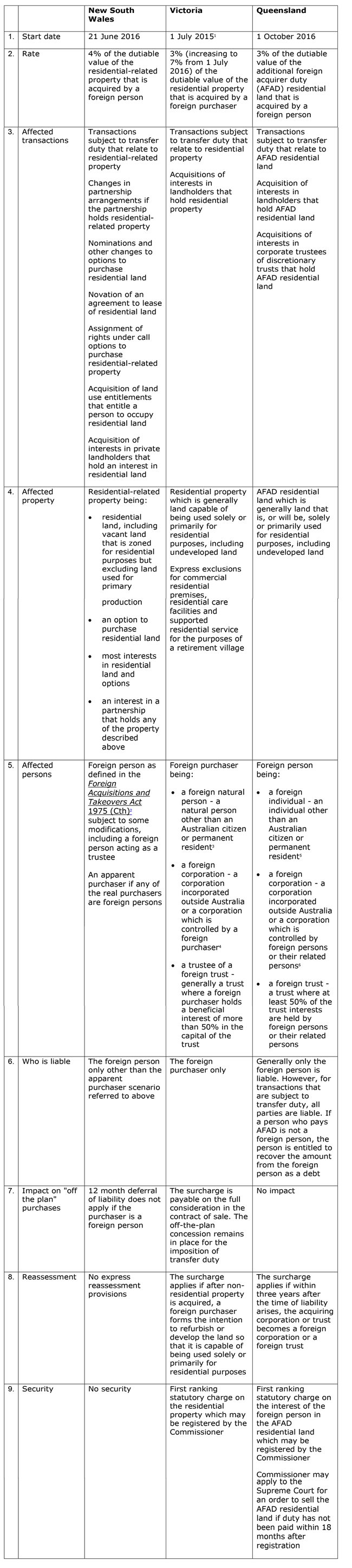

Stamp duty surcharges in New South Wales, Victoria and Queensland

The key points are:

- The surcharge will generally apply to transactions involving residential land that are already subject to stamp duty and will be calculated in a similar manner. It will apply to direct and indirect acquisitions of residential land by foreign investors.

- Residential land includes developed land and undeveloped land which is intended to be developed for residential purposes. The provisions should not apply to commercial residential premises such as hotels, motels and serviced apartments.

- In Queensland, all other parties to the transaction are jointly and severally liable with the foreign investor for the surcharge, whether or not those other parties are foreign investors themselves.

- In Victoria and Queensland, the Commissioner will have express powers to reassess transactions that were initially not subject to the surcharge in certain circumstances.

- The "off the plan" concessions in New South Wales will cease to apply to foreign investors. The "off the plan" concession in Victoria remains unaffected, although the surcharge itself is calculated on the full consideration paid under the contract of sale.

- Victoria and Queensland have introduced first ranking statutory charges over the land to secure the payment of the surcharge.

- New South Wales and Victoria have clear transitional provisions which generally exempt options and contracts entered into before the relevant commencement date. The transitional provisions in Queensland are not as certain and we understand that the Queensland Office of State Revenue will shortly publish a ruling to provide more certainty.

- In Victoria, if a contract was entered into before the relevant commencement date but a nomination occurs after the relevant commencement date, the nominee will be subject to the foreign purchaser duty surcharge if they are a foreign purchaser.

The table below describes the principal features of the stamp duty surcharges in each state.

[1] The surcharge has been in effect since 1 July 2015, however the increased rate and certain other amendments apply from 1 July 2016.

[2] Foreign Acquisitions and Takeovers Act 1975 (Cth)

[3] Includes a New Zealand citizen living in Australia.

[4] Control is considered to be control of more than 50% of the voting power or potential voting power, or holding an interest of more than 50% of the shares. The Commissioner can make a determination that a person has a controlling interest in the company if the person has the capacity to determine or influence the outcome of decisions about the company’s financial and operating policies.

[5] Includes a New Zealand citizen living in Australia.

[6] Control is considered to be control of at least 50% of the voting power or an interest in at least 50% of the issued shares of the corporation.

New land tax surcharge in 2017 for foreign investors in New South Wales

From the 2017 land tax year, a new land tax surcharge will apply at the rate of 0.75% of the taxable value of residential land owned by a foreign person. The surcharge will be assessed separately in relation to each parcel of land owned by the foreign person and is payable in addition to the current land tax already payable.

There will be no tax threshold or any principal place of residence exemption available to land held by foreign persons.

Absentee owner land tax surcharge to increase in Victoria in 2017

Since 1 January 2016, an absentee owner has had to pay a land tax surcharge of 0.5%. This surcharge will increase to 1.5% on and from 1 January 2017. The new rate of land tax payable by absentee owners will apply to all non-exempt properties in Victoria.

An absentee owner includes an absentee individual, an absentee corporation or an absentee trust:

- an absentee individual is any individual who is not an Australian citizen or permanent resident, does not ordinarily reside in Australia and was absent from Australia on 31 December of the year prior to the tax year or for more than six months in total in the calendar year prior to the tax year

- an absentee corporation is a corporation that is incorporated outside Australia or in which an absentee person has a controlling interest. A person will be deemed to have a controlling interest where they hold more than 50% of the shares in the corporation, can control the composition of the board of the corporation or can cast more than 50% of the votes at the corporation's general meeting. Where the absentee owner is a corporation that was incorporated in Australia, the treasurer may exempt that corporation from the surcharge in certain circumstances

- an absentee trust is a fixed trust, a unit trust or a fixed trust which has at least one beneficiary who is an absentee person

This is commentary published by Colin Biggers & Paisley for general information purposes only. This should not be relied on as specific advice. You should seek your own legal and other advice for any question, or for any specific situation or proposal, before making any final decision. The content also is subject to change. A person listed may not be admitted as a lawyer in all States and Territories. © Colin Biggers & Paisley, Australia 2024.