This article was originally authored by Toby Blyth. For further details or assistance, please reach out to Michael Bracken.

In brief - Australia is moving closer to having a new corporate collective investment vehicle (CCIV)

The Australian Government has released for consultation the first tranche of the Bill and explanatory materials for the CCIV. In 2017 and early 2018 Australian Treasury issued consultation papers for a CCIV.

The forebear for a investment fund cell company is the protected capital cell insurance captive (

PCC), which has had a relatively long life in the offshore insurance market. A review of the PCC provides usefull insight into the CCIV framework and the obligations and liabilities in the structure.

PCCs are a form of insurance captive developed in the sophisticated offshore insurance market some decades ago. In many respects, they can be seen as a proto-CCIV, and it is likely that regulators have seen the experience of PCCs and adopted certain aspects of them.

A captive insurance or reinsurance programme is a self-organisation system where a company sets up its own insurance company to fund and manage its retained risks.

The simplest form of captive is a single-parent captive insurer. The captive insurance company is capitalised by the sponsoring corporation buying the equity of the captive. For a CCIV capitalisation will largely occur through external investors.

The captive then invests those funds from the sale of its equity in low-risk, marketable securities that function as risk reserves. The risk exposure for a captive is the key driver for the PCC structure, as the legal segregation of assets and liabilities at a cell level supports the risk exposure and business at the captive level.

The sponsoring company pays premiums to the captive company (which is the insurer), who in return insures against risks that the sponsor wishes to retain and self-insure.

The captive can be managed by the sponsoring corporation, independent managers or a specific captive-management firm.

Rent-a-captives

Industry identified (in the late 1990s) that a corporation may wish to gain the benefits of having a captive, but may not have the resources or willingness to actually create one.

The rent-a-captive is maintained, owned and managed by the insurer/reinsurer, but for the benefit of those companies without the resources to create their own captive. The rent-a-captive itself is usually a reinsurance company.

The participants themselves do not make any equity investment and therefore do not own any part of the rent-a-captive's equity.

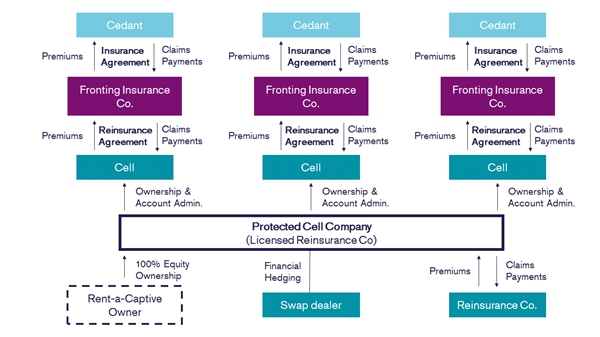

The below framework is useful in understandiung the framework for PCCs and segregation.

Source: Adapted from Structured Finance and Insurance: The ART of Managing Capital and Risk, C Culp, Wiley Finance, 2006

PCCs reduce overheads

The benefits of having more than one firm in each PCC structure is clear - it reduces overheads by sharing the costs amongst all the participants.

PCCs offer insolvency protection

A key driver of PCCs was insolvency. Although there was no intended risk transfer between the insurers sharing the captive, if a cedant submitted a claim that exceeded the resources in their notional account maintained by the captive as the insurer, there was a risk that the captive's entire asset base was available to satisfy the contractual claim.

PCCs are largely the same as a rent-a-captive, the only difference being that all customer accounts are legally segregated in such a way that the segregation will be maintained even in insolvency. They mirror in many ways the CCIV structure.

Business and risk focus in CCIVs

In providing for legal segregation of assets and liabilities, there can be a targeted business focus for a cell and the corresponding captive. For the insurance industry, similar to the funds management industry, this allows for better economies of scale across the capital and resources of the insurance business.

The Australian Treasury has prepared the following summary comparison table for the proposed CCIV regulatory structure for the cell/sub-fund.

Source: A copy of the original table is available on the Australian Treasury website under the CCIV Slides link

here.

References

Banks, R,

Alternative Risk Transfer, Wiley Finance 2004

Adkisson, D,

Captive Insurance Companies, iUniverse 2006

Stewart, H & Cantley, B,

US Captive Insurance Law, iUniverse, 2015

Wöhrmann, P & Bürer, C,

Instrument der alternativen Risikofinanzierung, Schweizer Versicherung 7 - 2001, p 14

This is commentary published by Colin Biggers & Paisley for general information purposes only. This should not be relied on as specific advice. You should seek your own legal and other advice for any question, or for any specific situation or proposal, before making any final decision. The content also is subject to change. A person listed may not be admitted as a lawyer in all States and Territories. © Colin Biggers & Paisley, Australia 2024.